The invasion of Ukraine in February 2022 prompted the US Treasury Department to impose unprecedented sanctions on Russia, to hold it “accountable for its premeditated and unprovoked invasion”.

The aim was to prevent Russia from “prop[ing] up its rapidly depreciating currency by restricting global supplies of the ruble and access to reserves that Russia may try to exchange to support the ruble”. In other words, Russia wouldn’t be able to sell enough US dollars in the foreign exchange market to buy up Russian currency and bolster its value.

Indeed, US secretary of the treasury Janet Yellen called this an “unprecedented action” that would “significantly limit Russia’s ability to use assets to finance its destabilising activities”.

Freezing a sovereign country’s dollar holdings (Russia’s in this case) is a seismic event. It risks accelerating a move away from use of the US dollar for trade or investment by countries that have different geopolitical interests than the US, such as China or the Gulf states.

In fact, several governments outside the west are exploring ways to reduce their exposure to the dollar. Russia is currently settling a quarter of its international trade using Chinese renminbi, and its bilateral trade with China is almost entirely settled in the two countries’ respective currencies.

In March 2023, China settled a payment for UAE gas in its own currency rather than US dollars for the first time. Then in November, China and Saudi Arabia signed a currency swap agreement, citing a desire to expand the use of their currencies.

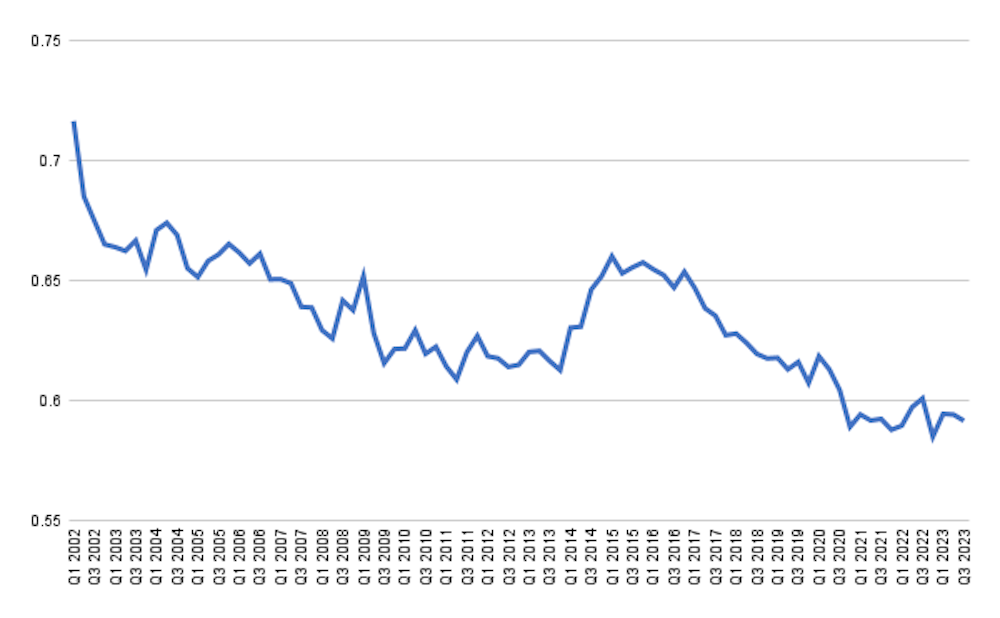

There are more troubling signs for the US dollar. Even though central banks’ foreign exchange reserves have been growing steadily year-on-year for more than 20 years, the percentage held in US dollars reached its lowest point in the fourth quarter of 2022, as this chart shows:

US$ held by central banks

This is not a blip. It is the culmination of a long negative trend that has seen the US currency’s share in foreign reserves held by central banks fall from over 70% in the early 2000s to under 60% today.

While the drop is not dramatic, it’s significant and indicative of a negative trend for the dollar that reflects several developments – economic but also geopolitical.

Leaving the US behind?

The US economy’s share in the world’s output is falling as emerging economies, especially China, continue to outgrow the US and its western partners. China, the US’s biggest economic competitor, is now the main trading partner to more than 120 countries, with exports amounting to more than US$3.6 trillion (£2.8 billion). This risks leaving the US behind in the race for global trade dominance.

Over the last 20 years, China’s share of the global economy has more than doubled from 8.9% to 18.5% while the US’s share declined from 20.1% to 15.5% in purchasing power parity terms (which compare prices of specific goods to determine currency purchasing power).

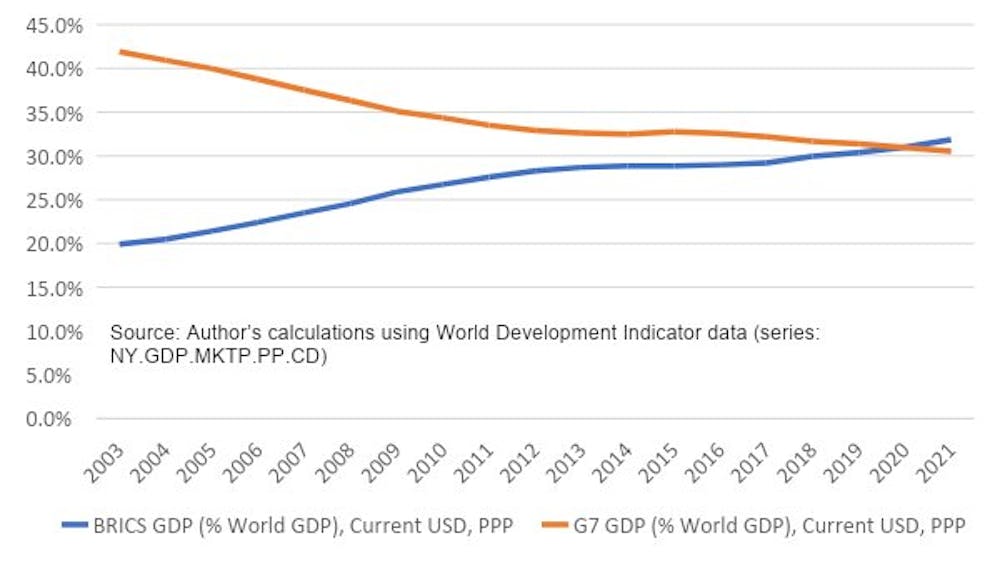

Last year, the Brics economies (fast-growth developing countries Brazil, Russia, India, China and South Africa) overtook those of the G7 (developed economies US, Canada, UK, Germany, France, Italy, Japan and Germany) based on their share of world GDP in purchasing power parity terms.

GDP: G7 v Brics

As more countries join the Brics, it will give the group even more economic clout.

Meanwhile, the US economy’s global GDP share is falling and its debt is hitting new heights as it issues more Treasury bills, notes and bonds to fund current government spending. The US national debt stands in excess of US$33 trillion, or 123% of the country’s annual output. Inflationary shocks followed by interest rate increases have made servicing this debt very expensive for US taxpayers, repeatedly raising the risk of a debt default in recent years.

There is no doubt the US dollar still dominates world markets right now, accounting for most of the transactions in international trade. Its share in the foreign exchange market is colossal at 88% of transactions, and it remains the most widely held “international reserve” by central banks who want to ensure they can cover their countries’ imports and support the value of their own currencies.

But the centrality of the US currency since the second world war has not always been welcome –– certainly not by US foes and sometimes not even by its friends. Valéry Giscard d’Estaing, the 20th president of France and a finance minister in the 1960s, called the dollar’s reserve status an “exorbitant privilege” for the US. He probably meant that demand for US assets from abroad was so high that it could borrow easily at favourable terms to finance its current account deficit –– a privilege not available to other nations.

Current global geopolitical and economic shifts could now see this exorbitant privilege challenged. The refusal of Russia’s Brics partners and many UN nations to undertake western-style sanctions against Russia is evidence of the limitations the west faces in exerting geopolitical influence.

And from an economic perspective, China as the world’s top trader and Russia as one of the world’s richest countries by energy reserves have amassed large gold holdings which could replace some US dollar uses. Both are looking to work with other countries, including those in the Gulf region, to reduce reliance on the US dollar.

Challenger currencies

Convincing non-western investors to use a “challenger currency” – whether the Chinese renminbi or a Brics currency – could become easier following the US Treasury’s freezing of Russian assets. And these switches could accelerate if the US decides to seize the frozen Russian assets.

It’s increasingly clear that, as non-western countries assert themselves in the world’s economic arena, geopolitical divisions with the west will cause additional friction. As a result, the US dollar’s role is almost certain to become more limited than it has been at any time since the end of the second world war.

![]()

Alexandros Mandilaras does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.