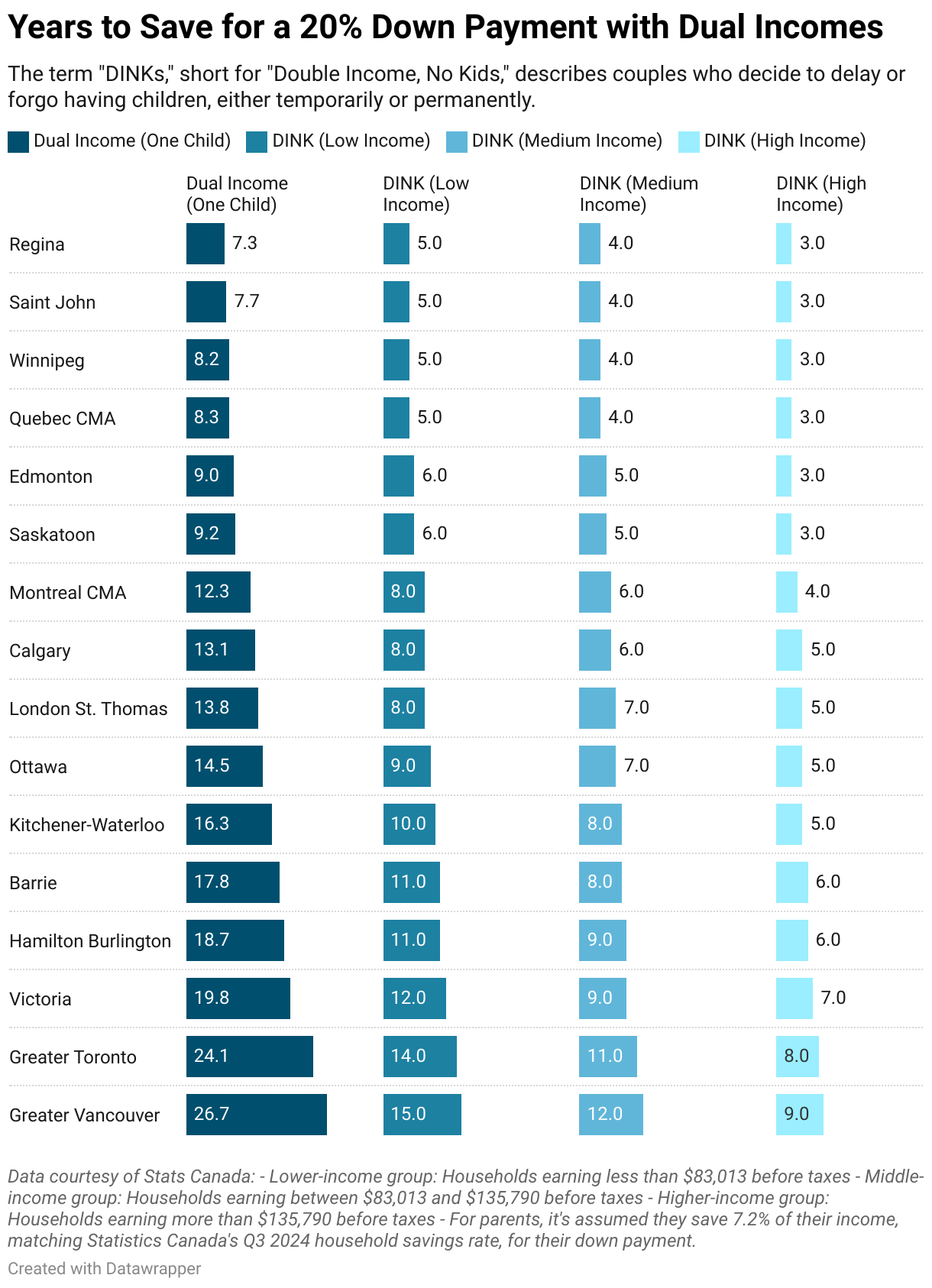

The term “DINKs,” short for “Double Income, No Kids,” describes couples who decide to delay or forgo having children, either temporarily or permanently. This demographic is growing as more people prioritize economic opportunities and stability over parenthood, and their financial advantage in the housing market is worth noting.

But no matter what your family unit looks like, saving for a 20% down payment on a home is a significant milestone for Canadian homebuyers—and for good reason. It’s often considered the gold standard for aspiring homeowners, offering several financial advantages. Not only does it significantly improve your chances of securing a mortgage by demonstrating financial stability and reducing risk for lenders, but it also allows you to skip costly mortgage insurance premiums, potentially saving thousands of dollars over the life of a loan. Perhaps most importantly, it accelerates your path to paying off the mortgage entirely, helping you build equity faster and providing greater financial flexibility down the line. However, reaching that 20% goal can feel daunting, depending on where you live, your financial situation, and whether or not you have children.

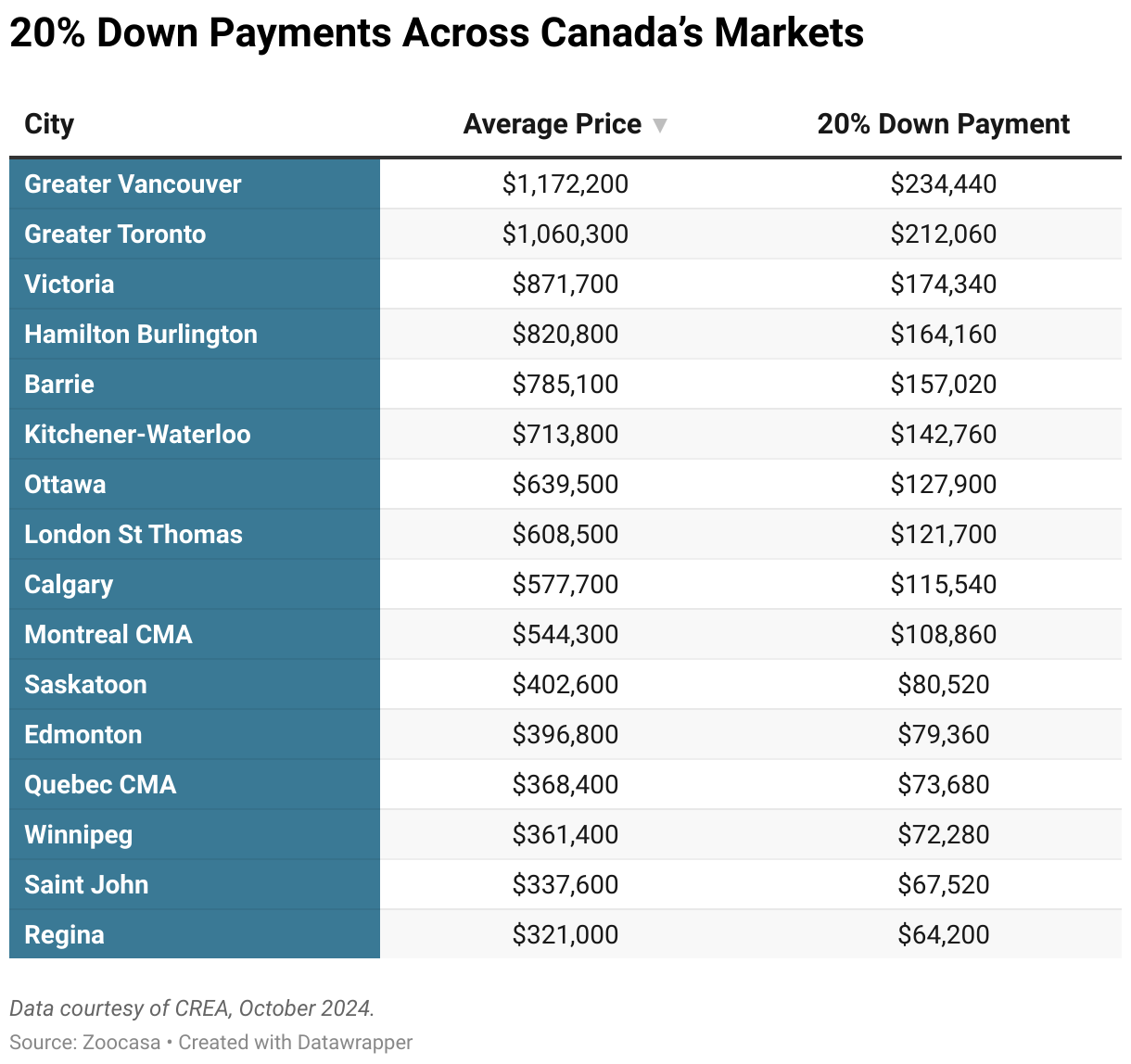

According to 2022 data from Statistics Canada, the median after-tax income for two-parent households with children is $122,000, while couples without children have a median after-tax income of $96,700. Using the Canadian Real Estate Association’s (CREA) October 2024 report on average home prices, we estimated how long each group would save for a 20% down payment.

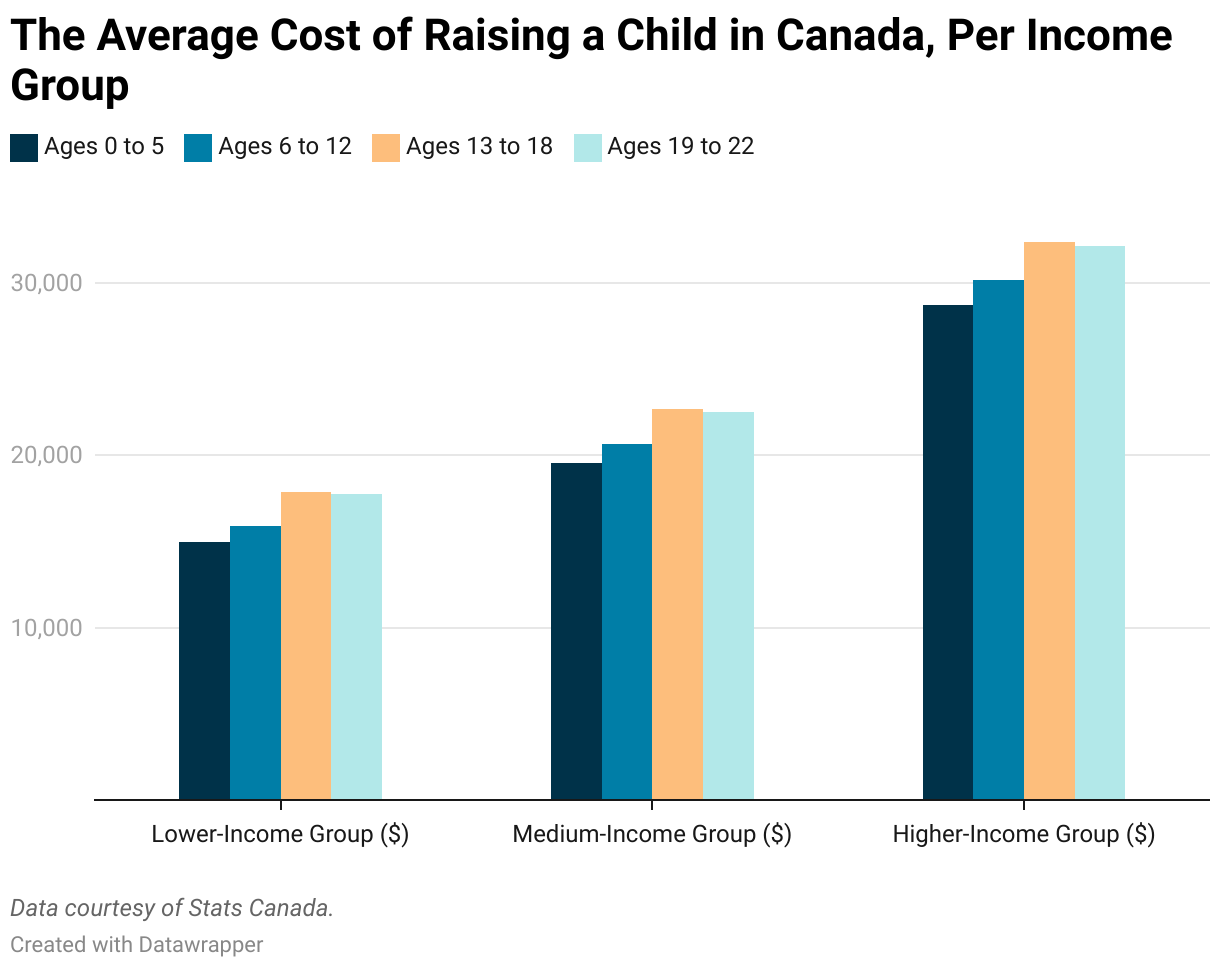

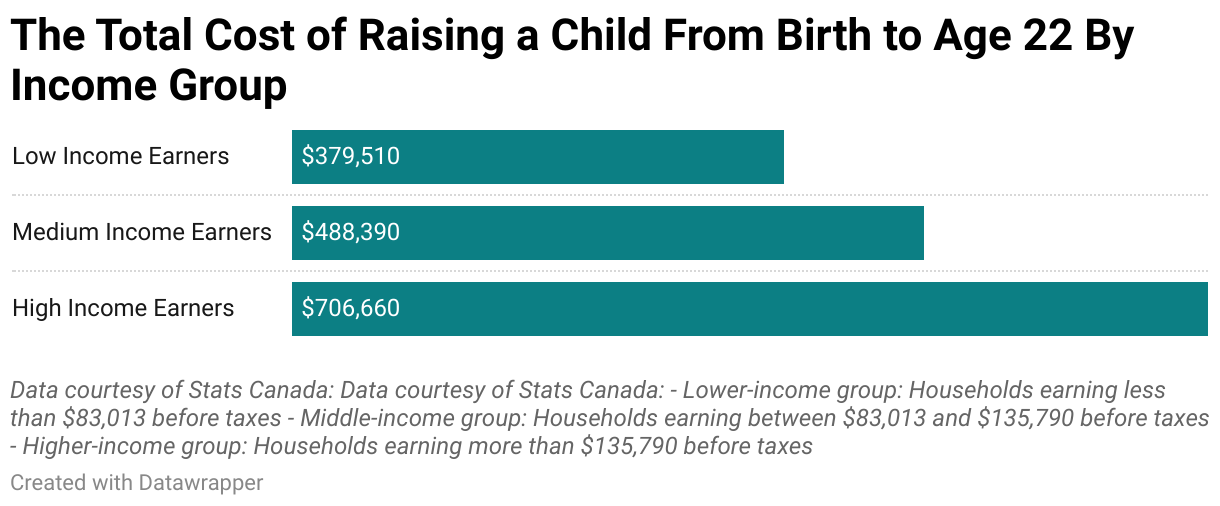

For parents with children, it’s assumed they save 7.2% of their annual income, consistent with Statistics Canada’s Q3 2024 household savings rate, to build their down payment. For couples without children, we calculated how much they might save by redirecting the annual costs typically associated with raising a child (low, medium, and high-income scenarios) toward their down payment, accumulating savings year over year. This comparison highlights the different financial pathways each group navigates toward homeownership.

Saving for a Home: How Kids Change the Timeline

In Canada, the time it takes to save for a down payment varies widely depending on the region and household circumstances. For dual-income couples with one child, about 37.5% of cities make it possible to reach a 20% down payment within 10 years. Cities like Saskatoon, Edmonton, Winnipeg, Regina, Saint John, and Quebec City are among the most affordable, where housing prices make saving more manageable and can help a dual-income couple with a child reach the goal in less than a decade.

In contrast, high-income, dual-income couples without children have a much faster path to homeownership. In the most affordable regions, they can save for a 20% down payment in just three years, making it 70% faster to save, accounting for the cumulative costs of raising a child from birth to age three.

Meanwhile, 25% of regions, such as Calgary, London St. Thomas, Montreal, and Ottawa, fall in the 10 to 15-year range for a dual-income couple with a child. These areas are slightly pricier but still within reach for many families.

Things get more challenging in cities like Victoria, Kitchener-Waterloo, Hamilton-Burlington, and Barrie, where saving for a down payment takes between 15 and 20 years. These markets have seen significant price growth in recent years, making it harder for families to keep up. Greater Vancouver and Greater Toronto are at the farthest end of the spectrum, where saving takes over 20 years. For families in these high-cost living areas, the dream of owning a home can feel increasingly out of reach.

Double Income, No Kids: Saving Made Simple

Saving money is much easier for middle-income earners without children. About 25% of cities allow this group to save for a down payment in less than five years, while a majority (62.5%) fall within the five—to 10-year range. Only 12.5% of cities extend this to 10 years for these households, showing just how much financial flexibility changes when the cost of raising children is removed.

Even in pricier markets like Toronto and Vancouver, saving can still be quicker for low-income earners without kids. In Toronto, low-income couples can save for a down payment 10 years faster than a dual-income couple with a child, while in Vancouver, it’s 11 years quicker. To put this into perspective, a couple without kids at age 25 could save enough for a down payment in Toronto by age 36. For a couple with a child, that milestone might not come until 49, illustrating the significant financial strain children can add.

Even in the most expensive regions, raising a child for a high-income family over nine consecutive years could cover a 20% down payment in Greater Vancouver or eight years in Toronto. For slightly less costly areas like Hamilton-Burlington or Barrie, it would take six years, while in Victoria, it would take seven years.

The Price of Parenthood in Canada Today

Unfortunately, this financial stress isn’t limited to housing costs. A recent Angus Reid survey conducted for Willful highlights challenges as Canadians head into the end of 2024. Nearly half (42%) of respondents say they feel worse off financially than at the start of the year. Everyday expenses have become so overwhelming that 48% admit dipping into their savings to stay afloat.

Parents, in particular, are feeling the strain, with 52% reporting that their financial situation has worsened since January 1. The numbers are even more startling for parents with young children—83% say they’ve had to delay major financial decisions like saving for the future or planning for significant expenses. This is significantly higher than the 72% of Canadians overall who are delaying financial choices.

The primary culprit behind this stress? Inflation. A staggering 90% of parents worry that rising costs will derail their financial goals. With day-to-day family needs taking priority, over half (54%) of parents have already used their savings in the past year to cover basic living expenses.

What to Consider Before Growing Your Family

Having children is one of the most significant decisions you’ll make, and financial preparedness is a key part of the equation. Here are some important considerations to keep in mind:

Budgeting for Maternity or Parental Leave

In Canada, maternity and parental leave provide income support but often replace only a portion of your regular salary. Through Employment Insurance (EI), you may receive 55% of your earnings for up to 12 months or 33% for an extended 18-month leave. While some employers offer top-ups to cover a greater percentage of income, not all do. Planning for reduced earnings during this time can help alleviate financial stress and allow you to focus on your growing family.

Renting vs. Buying a Home

If you’re currently renting, consider whether transitioning to homeownership before having kids aligns with your financial goals. Renting provides flexibility, but buying a home offers long-term stability—mainly as your family grows and your needs evolve. Larger living spaces typically come with higher costs, so deciding whether to rent longer or prioritize homeownership before starting a family can significantly impact your financial plans.

Considering an Investment Property

Another strategy is purchasing an investment property in a more affordable market, also known as “rentvesting”. This allows you to build equity while renting or living in your current home. Rental income from the property can offset costs, and the equity you build could later help fund major expenses like a larger family home, educational savings, or an extended parental leave.

With all this in mind, you can create a balanced plan that supports your family goals while maintaining financial stability. For expert insights on real estate planning as you grow your family, contact an agent at Zoocasa today.

The post No Kids, No Problem: How DINKs Outpace Families With Children in Home Savings appeared first on Zoocasa Blog.