Building home equity is one of the greatest benefits of homeownership. Home equity gives you the financial freedom to borrow against your home for major expenses, invest in other opportunities, or enjoy greater financial security as your property value grows.

Your home’s equity is the difference between its current market value and the remaining balance on your mortgage. If you have already paid off your mortgage, then you have 100% equity in your home. While you cannot completely control your home’s current market value, there are strategies to increase your equity and accelerate mortgage payoff, ultimately giving you full ownership of your home.

Invest in Home Improvements and Upgrades

The size, location, upgrades, amenities, number of rooms in your home, and other factors help determine your home’s current market value. If you have an older home with outdated appliances, the home’s market value will likely be less than a home that is newer with renovated rooms and updated appliances.

For this reason, many home sellers invest in upgrades and renovations before listing their homes on the market. If you want to build equity faster, then making improvements in some key areas of your home can help. Before jumping into renovations, consider which rooms and features are highlights of your home and which areas will be used the most. The type of renovation you invest in can significantly impact your home’s equity, so it’s important to plan strategically rather than spend impulsively.

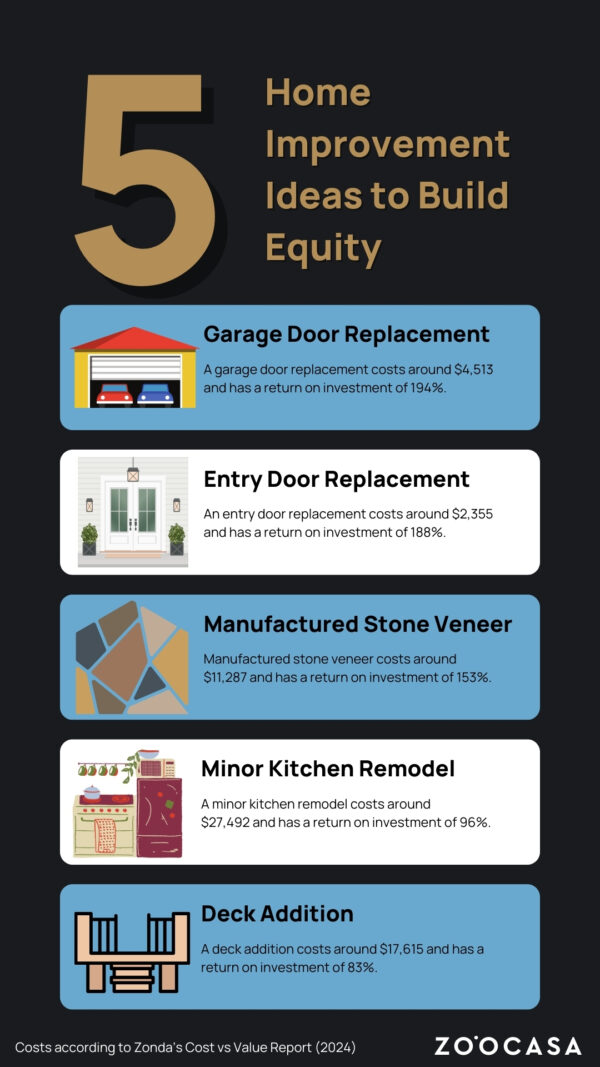

Zonda’s 2024 Cost vs. Value report ranks home renovations by return on investment, helping homeowners determine which parts of their home to focus on to increase their home’s value. Here are some key upgrades to consider that offer a high return on investment:

- Garage Door Replacement

- Minor Kitchen Remodel

- Deck Addition

- Bath Remodel

- HVAC Conversion

- Window Replacement

Environmental upgrades are also becoming increasingly important and popular among home buyers. Freddie Mac research shows that energy-efficient homes sell for 2.7% more than unrated homes, with higher-rated homes selling for up to 5% more. Environmental upgrades to consider include installing solar panels, energy-efficient windows, and LED lighting.

Prioritize Regular Maintenance and Upkeep for Your Home

Wear and tear on a home is natural after years of use, but there are ways to slow and even prevent this process. Keeping up with essential maintenance tasks helps extend the lifespan of your appliances and home features while preserving your home’s aesthetics. Regular upkeep also allows you to catch potential issues early, avoiding costly repairs in the future.

Weekly maintenance tasks:

- Wiping down countertops and tables

- Vacuuming and sweeping floors and carpets

- Disinfect toilets and showers

- Clean mirrors and windows

Monthly maintenance tasks:

- Clean sink and shower drains

- Check HVAC filters

- Declutter living room and bedrooms

- Clean out your fridge

Seasonal maintenance tasks:

- Clean gutters

- Inspect the roof for damaged shingles

- Check faucets for leaks

- Trim trees and bushes

- Clean the inside of your dishwasher

- Inspect water heaters

Put Down a Larger Down Payment

Beyond regular upkeep and renovations, you can build equity faster by paying off your mortgage sooner. One way to achieve this is by borrowing less. The size of your down payment directly impacts how much you owe to your lender, so increasing your down payment means borrowing less, which allows you to pay off the remaining balance more quickly.

Additionally, making extra payments toward your mortgage principal, either regularly or as a lump sum when possible, can further accelerate the process. By reducing your loan balance faster, you’ll save on interest over time and build equity at a much quicker pace.

Shorten Your Loan Term

Similarly, you can pay off your mortgage sooner by shortening your loan term. The typical loan term is 25 or 30 years, but if you can afford to have a higher monthly payment you can shorten the loan term. You’ll also benefit from paying less interest with a shortened loan term.

For example, with a benchmark price of $1,113,600, Toronto homeowners will pay $789,682 in interest for a 25-year mortgage. However, opting for a 30-year mortgage would result in $186,263 more in interest compared to the 25-year term.

Want to learn about market conditions in your area Give us a call today to speak to a local real estate agent who can guide you through the exciting homebuying process.

The post Smart Strategies to Build Equity in Your Home Faster appeared first on Zoocasa Blog.