The Reserve Bank of Australia has delivered a shock 12th rate hike since May last year, deciding to lift interest rates in a bid to tackle persistently high inflation.

The central bank chose to lift the cash rate target by 25 basis points to 4.10 per cent, surprising the financial markets and the majority of economists who predicted a pause on rate hikes in June.

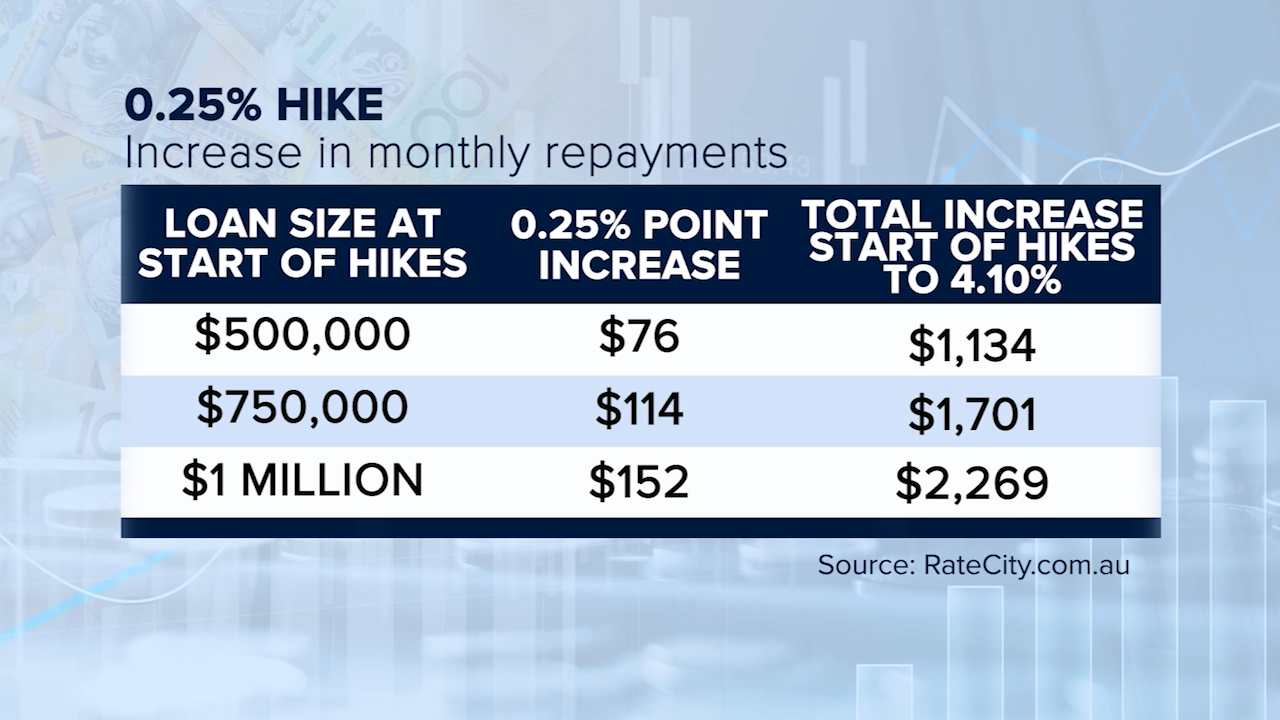

For the average Australian mortgage, today's rate hike represents an additional $1,264 in mortgage repayments since the cash rate was 0.10 per cent in April 2022.

READ MORE: Australians bracing for another rate rise as mortgage arrears spike

Australia's base interest rate level is now at it's highest point since April 2012.

In his monetary statement RBA Governor Philip Lowe said today's increase was a necessary step to contain inflation.

"Inflation in Australia has passed its peak, but at 7 per cent is still too high and it will be some time yet before it is back in the target range," Lowe said.

"This further increase in interest rates is to provide greater confidence that inflation will return to target within a reasonable timeframe."

Lowe said there were signs that the economy was slowing, but inflation was still a way off the central bank's target band of between 2 and 3 per cent.

"The combination of higher interest rates and cost-of-living pressures is leading to a substantial slowing in household spending," he said.

"Housing prices are rising again and some households have substantial savings buffers, although others are experiencing a painful squeeze on their finances."

READ MORE: National 'misery index' up 220 per cent as Aussies struggle

He said the RBA remains "resolute" in bringing down inflation, forecasting that further hikes may be needed.

"Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will depend upon how the economy and inflation evolve," he said.

"The Board will continue to pay close attention to developments in the global economy, trends in household spending, and the outlook for inflation and the labour market.

"The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that."

Treasurer Jim Chalmers said today's decision would be hard to hear for millions of Australians, but said the it was not right to blame Australians for inflation-adding decision such as asking for pay rises or buying property.

"This will make life much harder for people with a mortgage," he said.

"I do expect that there will be a lot of Australians who find this decision difficult to understand and difficult to cop.

"Ordinary working Australians are already bearing the brunt of these interest rate rises, they shouldn't bear the blame too."

READ MORE: Aussie bank's grim prediction for millions of borrowers

Graham Cooke, head of consumer research at Finder, said the decision came as a shock to many.

"The RBA continues to operate in the dark, as our panel of economists are split on the bank's intentions," he said.

"Aussies with an average loan size of $577k will be spending over $15k more per year on their mortgage compared to what they were in April last year.

"That's an additional $1,200 every month – a huge amount of extra money to be forking out on your mortgage."

READ MORE: Free car rego for Victorian apprentices

RateCity.com.au research director Sally Tindall said many Australian households are facing a financial reality few could have forecast when rates were at the historic low of 0.10 per cent in 2022.

"Australia's twelfth hike in 14 months puts many borrowers into financial territory they never thought they'd see in the life of their loan, let alone in just over a year," she said.

"The RBA is increasingly starting to look like Fred Flintstone and Barney Rubble. It's doing what it can with a very blunt instrument.

"Some borrowers are well into the red with limited avenues out. Others are either splashing the cash or squirreling it away in the bank. At what point should the government reassess the instrument rather than the Board using it?

"In less than two weeks' time, the majority of borrowers will be charged a higher interest rate as a result of this RBA decision, yet, in many cases, the extra money won't come out of their bank accounts for another three months – depending on their bank."

Sign up here to receive our daily newsletters and breaking news alerts, sent straight to your inbox.