A woman cycling past the Bank of England.

A woman cycling past the Bank of England.Raising and lowering interest rates is the blunt instrument used by central banks to control economies.

Hiking the “base” rate increases the cost of borrowing, making both credit and investment more expensive. The idea is to put the brakes on the economy and curb the soaring cost of goods and services – known as inflation.

Bringing rates down is an attempt to have the opposite effect – stimulate growth by making borrowing cheaper, and in turn, encourage investment.

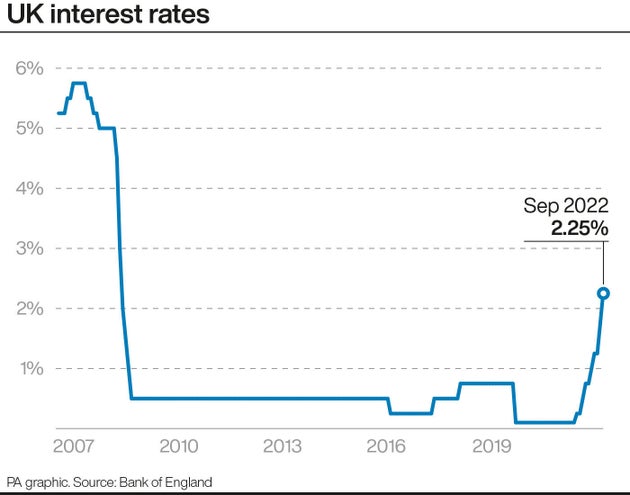

On Thursday, the Bank of England – the UK’s central bank – said that it would raise interest rates by 0.5 percentage points to 2.25%.

It marks the seventh consecutive rise since December last year, with analysts certain the move could be followed by more increases. It also indicated it believes the economy is already in recession.

As a sign of trouble in the economy, it means that rates are now at their highest level since 2008, when the banking collapse forced saw monetary policy makers slash the cost of borrowing.

Here’s what it means for households and why any gains will be modest.

Why are rates rising so much?

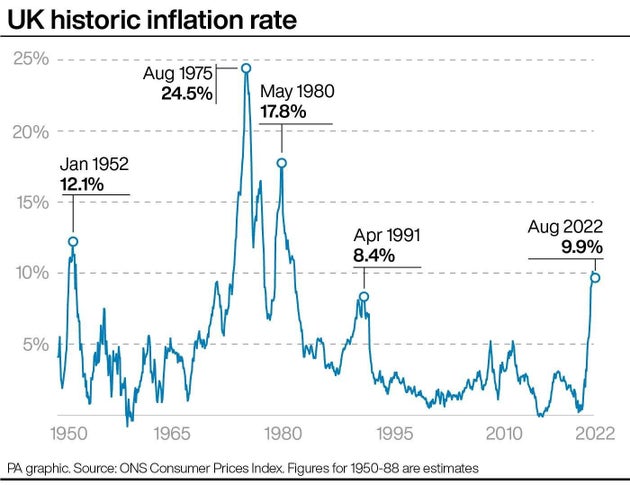

The Bank of England is tasked with keeping inflation under control, targeting 2% a year.

But in recent months inflation has started to run away. It hit 9.9% in August and despite government action to freeze energy bills is still expected to strike a new 40-year-high “just below 11%”, according to a new forecast from the Bank.

UK interest rates.

UK interest rates.Members of the Bank’s Monetary Policy Committee (MPC) said on Thursday that inflation is likely to sustain at high levels following the energy support for households, as it will boost many people’s spending power.

But by increasing interest rates, the Bank makes it more expensive to borrow money, so people are therefore likely to spend less.

If people – and businesses – are forced to spend less, demand will decrease, and prices will fall, or at least the rises will mellow.

How will the interest rate hike impact people?

Mortgages

The most obvious impact is that it will become more expensive for people to pay off their mortgages.

People taking out a new loan will soon be quoted a higher interest rate as a result of the Bank’s change.

And those whose mortgages are being renegotiated will likely have to deal with larger bills than they had in the past.

Trade association UK Finance said that the rate rise would mean mortgage borrowers whose deal directly tracks the base rate will see their payments increase by around £49 per month on average, adding up to nearly £600 annually.

NEW: Interest rates rise to 2.25%.

This Tory government has lost control of the economy.

By putting such huge unfunded and uncosted sums on borrowing they’re pushing up mortgage costs for everyone.

Their reckless approach is an immense risk to family finances.

— Rachel Reeves (@RachelReevesMP) September 22, 2022

The figures also showed that a borrower sitting on their lender’s standard variable rate (SVR) will typically see a monthly increase of just under £31, adding up to around £370 per year.

Nearly four-fifths (78%) of residential mortgages outstanding are fixed rates, meaning these borrowers will not see the immediate impact of the Bank’s base rate hike.

But, if they have been safely locked into their home loan for a while, they may find they get a shock when they do eventually re-mortgage. A year ago, it was possible to get an interest rate of less than 1% for two or even five years. Now even the best deals are in the region of between 4% and 4.5%.

Credit

Those with other types of debts will also feel the squeeze.

Anyone with an existing fixed-rate personal loan, credit card or car loan will be unaffected as the terms of their loan have already been agreed.

But new borrowers shopping around for credit may find the cost of debt higher. The cost to borrow on a credit card is already on the rise, with the average credit card purchase APR (which includes card fees) rising to an “all-time high” of 29.6% APR.

Why is the cost of living soaring so much?

Inflation is a measure of how much the price of the things that the average household buys is changing, with the Ukraine war compounded a crippling cost-of-living crisis where wages are failing to keep pace.

Inflation is likely to peak in October, largely due to the amount that people pay for the energy they use to run their homes. Energy prices will contribute around 40% of the inflation that the Bank is expecting in October.

Nevertheless, the Bank highlighted that the decision by Liz Truss’ new government to freeze energy bills at £2,500 for an average household means inflation will not soar as high as previously expected.

UK historic inflation rate.

UK historic inflation rate.Who benefits from the interest rate hike?

Savers will benefit a little from the rate hike as the banks they keep their money with are likely to increase the amount of interest they pay on deposits.

The average rates being offered on some savings accounts have reached their highest level in nearly a decade, according to Moneyfacts.co.uk.

However, many savings accounts have not seen their rates lifted yet towards the levels of interest rate rises.

Alice Haine, personal finance analyst at Bestinvest said: “While banks and building societies are quick to apply higher rates to debt, they can be a little slower to deliver the good news to savers.”

The impact of the increased interest that savers get will also be more than offset by inflation, which is more than decimating savings.

Related…

Source: Huff Post